Current State of the Automotive Industry

The current state of the industry could be described as transitory, with consumer preferences changing along with product offerings. OEMs are sort of all over the road, and frankly 2023 was a big year for the industry.

We are in a transition year for the auto world... really we are in a transition decade. Things are kind of crazy right now as manufacturers recover from supply chain issues and further invest in alternative powertrain technologies that lack the same profitability that they were accustomed to with gas-powered vehicles. 2024 will be a continuation of that, with the future kind of all over the road. Executives are having a hard time deciding which business units to invest in, and stockholders are wondering just how much value to place on hopeful EV startups.

"The EV transition is causing brutal volume unpredictability. Our company faces the challenge of managing these fluctuations with both delayed and compressed, aggressive launch timelines. Additionally, there's a significant issue with delayed payments across suppliers and OEMs, affecting cash flow" - Tier 1, Strategy, NA

Just recently Rivian has been under pressure to raise its stock price since it has plunged more than 90% since its IPO, and Fisker is (still) struggling to produce cash. Tesla also just dropped prices again (in the China market) in an attempt to lock in some more sales. It will be interesting to see where things are in 5-10 years.

Seraph (a consulting company that works in the automotive industry) recently released their North America and Europe Auto Industry Report, where consumer finances, market preferences, supply chain risks and the impacts of geopolitical events are covered. The report offers a bit of insight into what's going on right now, and this article covers some of the highlights. If you're interested in the full report, it is on their website.

Consumer Finances and Market Preferences

The report covers significant changes since last year from the consumer point of view:

- Vehicles are more affordable than the year prior

- OEMs talking about lower cost vehicles

- OEMs talking more about hybrids

- Vehicle inventories have been replenished

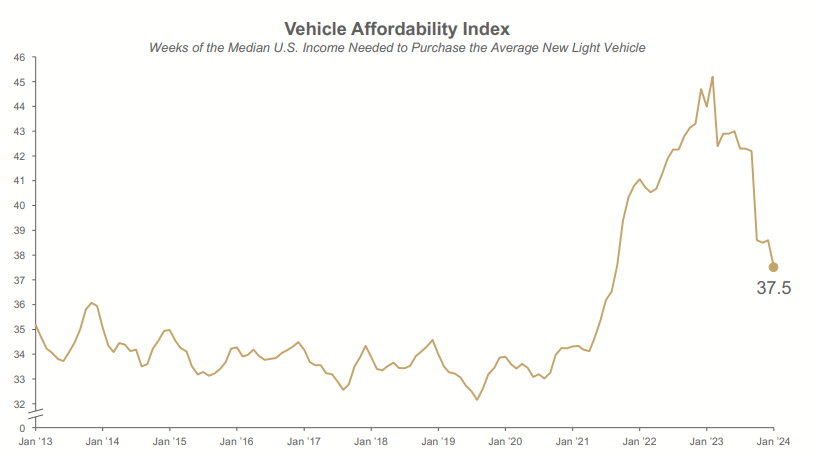

Vehicles have become more affordable in the U.S. over the last year, but still remain elevated compared to the norms of the last decade. Incentives from manufacturers are becoming much more common (up to 3.9% in Dec 2023 from 2.7% in Dec 2022).

Although the graph shows vehicles are cheaper now than previously, consumers may be more hesitant to spend because the data shows that 46% reference high prices as a reason why they aren't buying and 30% say interest rates are prohibitive. High fed rates means borrowing is still far more expensive than it was during COVID.

It's important to keep in mind that consumer credit card debt is still high, as well as auto loan delinquencies which are sitting at a 13-year high. The average "Joe Schmoe" consumer is still in a strained position it seems.

US EV Market

The top concerns within the market are affordability, range, and infrastructure. Government incentives regarding EV purchases have been reduced, and the average range of an EV is 250 miles compared to an ICE vehicle with 412 miles (paired with much faster re-fuel time).

To answer these concerns by buyers OEMs are really trying to reduce the price on EVs and spending money on developing new battery chemistries and lightweight materials. Many of the automakers have admitted defeat and agreed to adopt Tesla's supercharger network and associated NACS plug design. Since a 2022 peak, the price of Lithium has dropped nearly 80% due to increased production, which is still crazy (in my opinion) considering how much more demand there must be for it now compared to a couple years ago.

“EVs will only represent 30% market share, no matter how much progress BEVs make. The remaining 70% will be HEVs, FCEVs, and hydrogen engines. I think ICE cars will definitely remain.” - CEO and Chairman Akio Toyoda

Regarding the Detroit big three...

"Ford is recalibrating its EV strategy to move away from large, expensive EVs because high prices are the biggest barrier to convincing mainstream car buyers to go electric.” - Ford CEO Jim Farley

Input Costs and Supply Chains

Significant changes since last year include

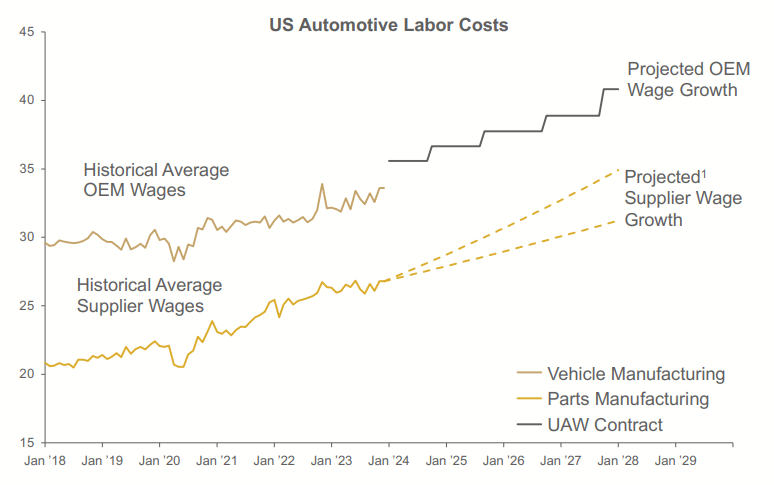

- Foreign OEMs responded to the UAWs Detroit 3 contracts by increasing wages for their workers, as the UAW mounts a campaign to organize at additional factories

- Lithium prices have declined substantially

- Ocean freight has increased

- In 2023, 34% of scheduled vehicle launches were delayed, leading to profitability issues

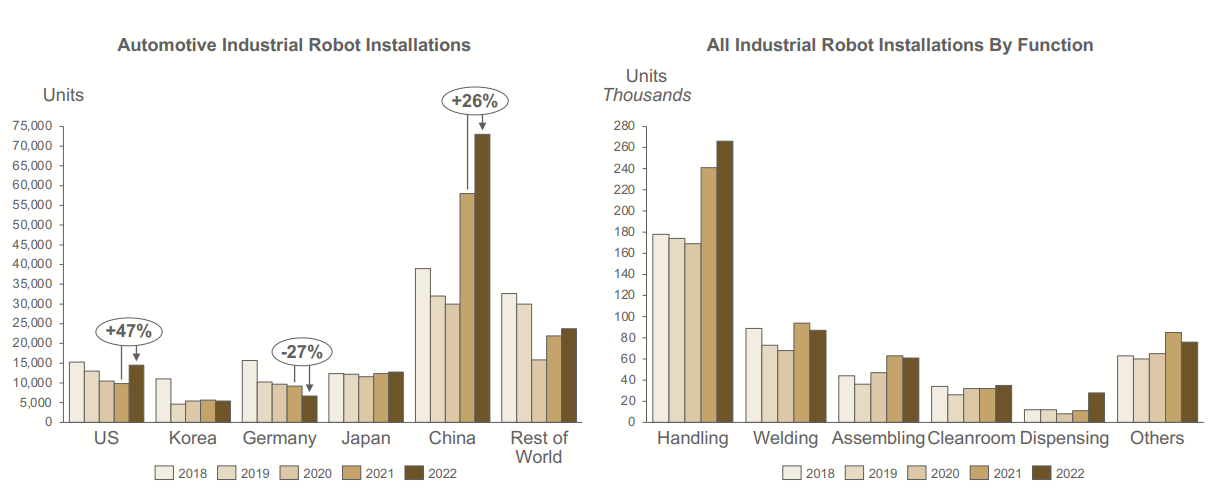

AI is proving to be useful for more than just looking up homework answers... apparently automakers are deploying it in their supply chain, where BMW is using it to oversee its robot production fleet and Tata Motors uses it to analyze historical data and market trends to predict demand. Toyota is using AI to help design the exterior of their concepts, which debatably takes away some of the fun. This trend isn't new, but the prevalence and ability of AI has definitely gained more speed over the last year.

Forecasting production scheduling and demand planning are popular with supply chain folks right now.

Leaving China is another trend, with 54% of respondents to Seraph's survey indicating that they were leaving China. Many of the respondents that are leaving China are headed to Mexico, Eastern Europe, and India. Some are headed for Southeast Asia and Africa, but Mexico gets the lion's share. This could be because of China's rising labor costs, geopolitical risks, or overall uncertainty regarding China's internal policy decisions that affect businesses.

The full report can be downloaded from Seraph's website. This article only covered a portion of it but the full report has many more interesting figures and graphs from all sorts of angles in the industry.

Thanks for reading - JWK

Comments ()