State of the Automotive Industry: Fall 2024

Trends that have emerged over the recent months highlight the risks of years of outsourcing to countries with cheap labor as well as concerns from the industry regarding the financial viability of BEVs in the short-term.

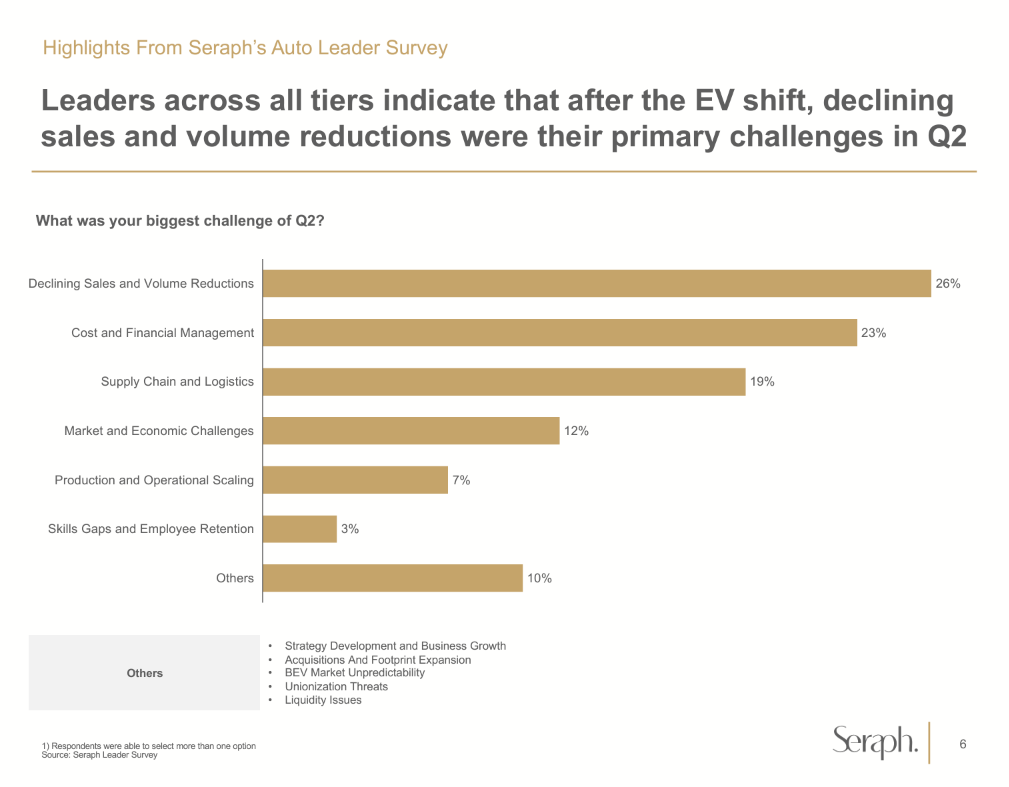

Seraph has recently released their latest report on the automotive industry, highlighting the challenges facing the industry and sentiment from leaders. This report accounts for responses from OEMs, Tier 1s, 2s, and 3+. Tier 1 suppliers account for 55% of the responses though, so keep that in mind. After covering previous industry reports in the past, it seemed fitting to create a highlight reel for this newest version as well. Trends that have emerged over the recent months highlight the risks of years of outsourcing to countries with cheap labor as well as concerns from the industry regarding the financial viability of BEVs in the short-term.

Auto Digest does not have any commercial relationship with Seraph.

Largest Trends

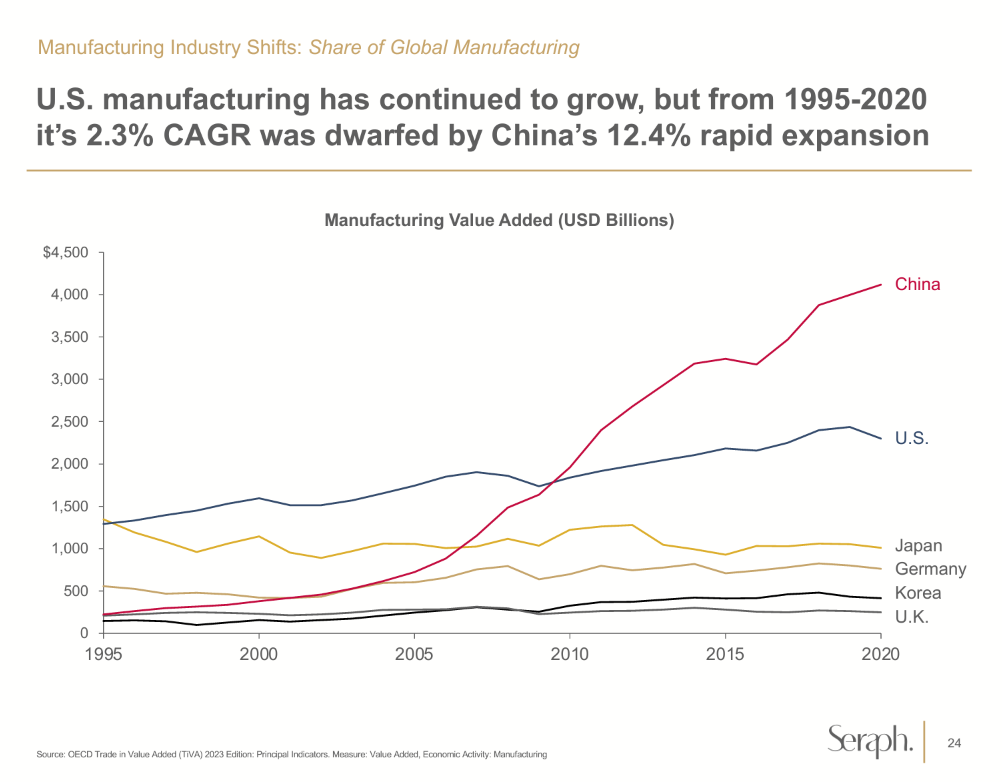

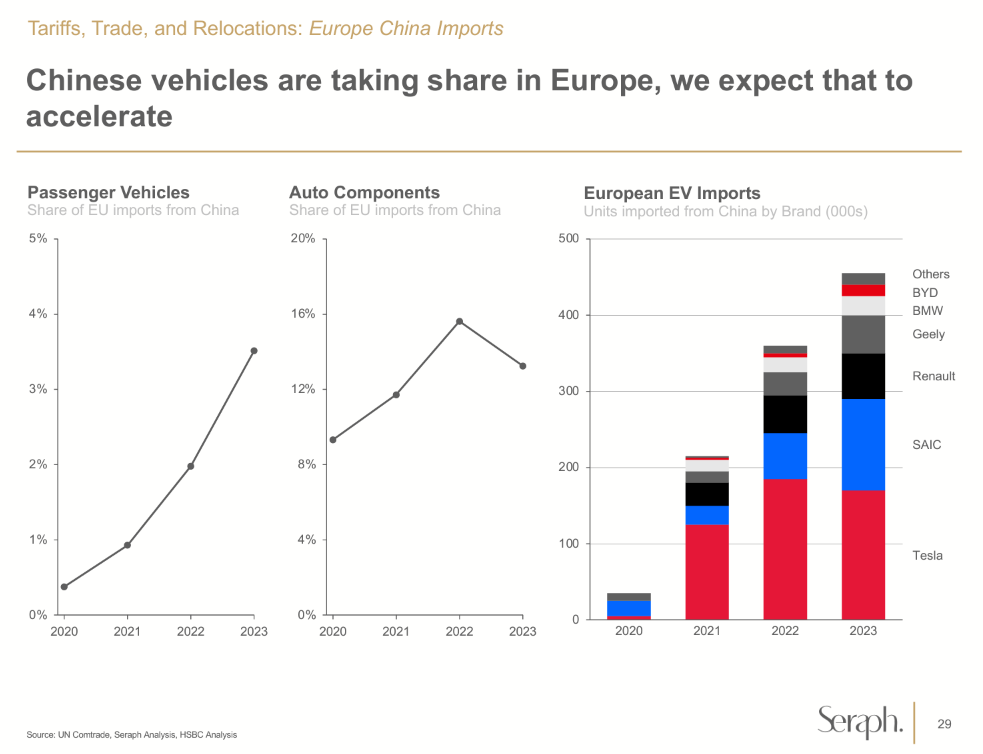

Immediate China Impact: Western governments around the world are concerned about technology products originating from China and are moving to restrict imports. Parts and software that support connectivity are facing the greatest scrutiny. Rising tariffs will erode cost competitiveness for export-driven China suppliers.

Navigating Painful Platform Shifts: A "platform" in the auto industry is sort of the baseline architecture that manufacturers will base multiple models off of to save money. Adopting existing platforms to become EV is expensive, and developing new EV-specific platforms is really expensive. Global EV manufacturing capacity has doubled, leading to surplus production capabilities since consumer demand is increasing but still lagging in relation.

Despite massive plant investments, charging options limit BEV adoption. After years of dwindling ICE investments, automakers are now spending money in this area again in an effort to get some short-term profit.

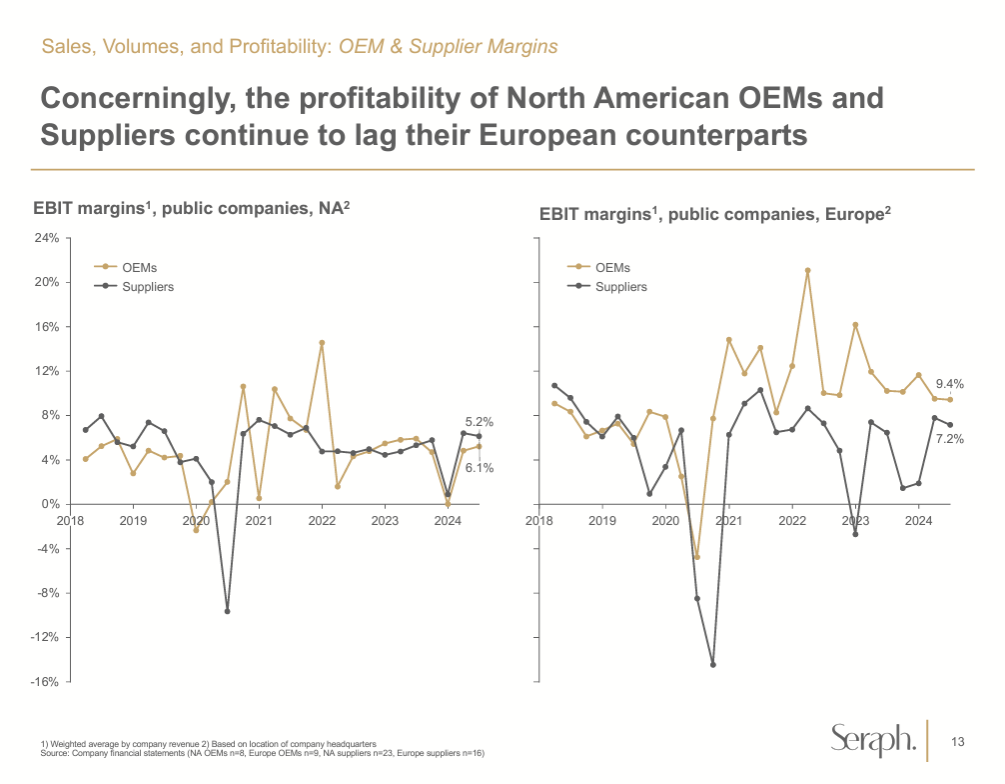

Strained OEM and Supplier Relations: Sustained disparities in profitability between OEMs and suppliers have strained commercial relationships. Increased debt financing costs thanks to higher interest rates are limiting investment in new technologies. Inadequate cash flow from low volumes is creating significant operational continuity risks.

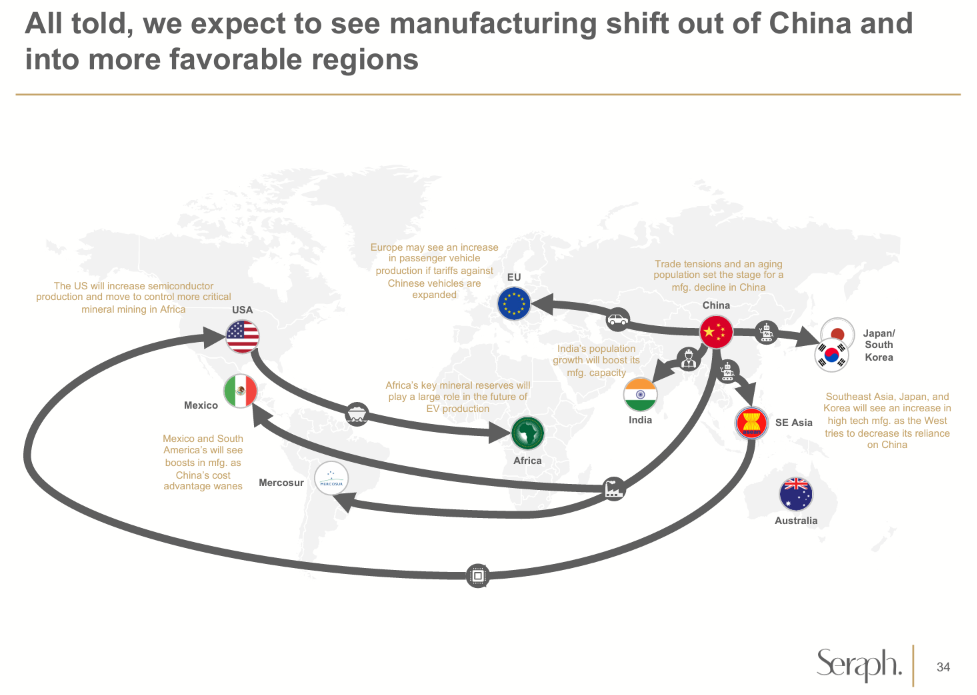

Aligning Strategy for Future Competition: Companies are beginning to implement a more localized supply chain to enhance supply chain responsiveness.

Relevant Charts

OEMs are pulling some EV investments back. The Stellantis Belvidere plant in Illinois has delayed the conversion to EV production until 2027, while Ford has also delayed the second plant construction of the Ford BlueOval SK plant in Kentucky, with no provided date for when it will resume. The GM and Samsung joint venture plant in Indiana was initially scheduled to begin operations in 2026 but has been pushed to 2027. BMW was supposed to break ground on a battery center in Mexico, but that has also been postponed indefinitely. EV investments are still happening in dramatic fashion, but automakers are having to be more diligent with their investments than they thought they would whenever they planned them a couple of years ago.

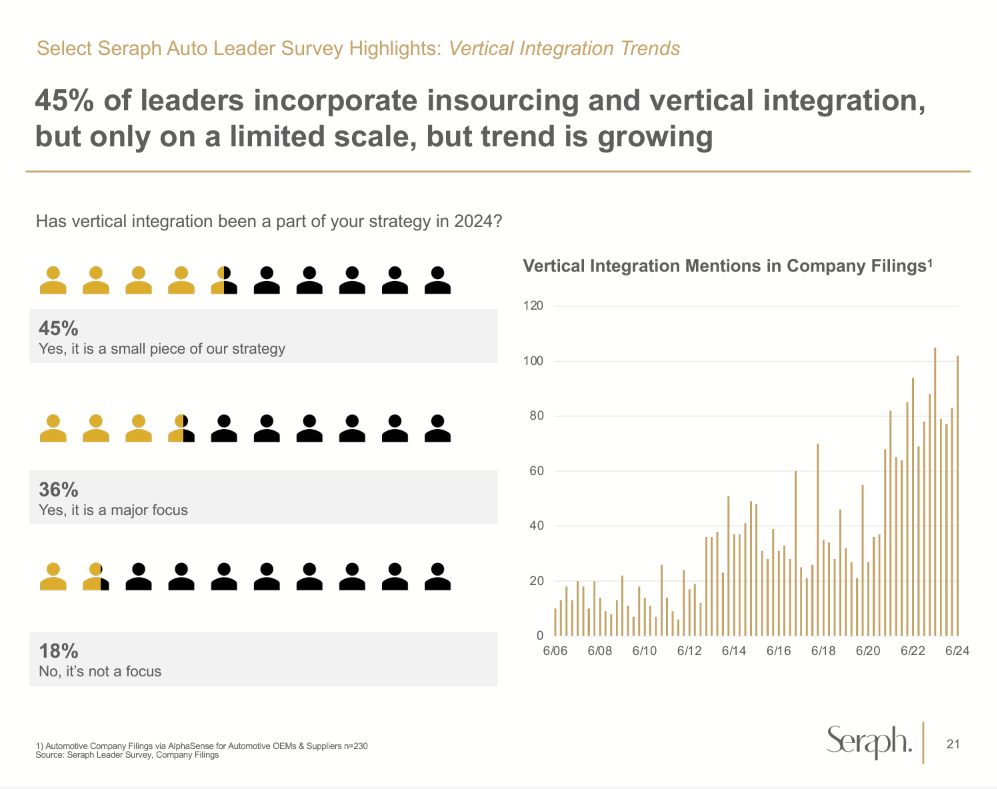

Insourcing in manufacturing refers to the practice of bringing production processes and operations back in-house rather than outsourcing them to external suppliers or contractors. Vertical integration involves expanding the company’s control over upstream (e.g., raw material sourcing) or downstream (distribution and retail) activities. Both of these strategies are becoming more popular. With all of the current geopolitical tensions in Israel, Ukraine, and Taiwan it's no surprise that leadership is concerned with moving some operations back in-house.

Industrial and Trade Policy: In the US, the Biden administration has invested ~$70B in clean energy manufacturing through the signing of the IRA and ~$53B in semiconductor manufacturing through the signing of the CHIPS Act. Over in Europe, the European Commission announced a tariff hike on Chinese EVs in an effort to push back on Chinese state subsidies that have enabled the Chinese to sell EVs for far less than their competition. The EU is set to vote on long-term Chinese EV tariffs by Oct 30th, with Germany and Spain already signaling their opposition.

Retail Side: Consumers are increasingly budget-conscious, with many looking for new vehicles priced under $30,000. However there is a limited supply in this price range, creating a disconnect between demand and availability. The average transaction price for a new car this summer was $47,716; that’s a nearly 30% jump compared to just five years earlier, according to Kelley Blue Book.

The full automotive industry report can be downloaded from Seraph's website. This article only covered a portion of it but the full report has many more interesting figures and graphs from all sorts of angles in the industry.

Thanks for reading - JWK

Comments ()